That's every year for the 5/1 ARM and every 5 years for the 5/5. These specific ARMs are best if the homeowner prepares on living in the house for a period higher than 5 years and can accept the modifications later on. The 5/25 mortgage is likewise called a "30 due in 5" home mortgage and is where the monthly payment and rates of interest do not alter for 5 years.

This implies the payment will not alter for the rest of the loan. This is a great loan if the property owner can endure a single change of payment during the loan duration. Home mortgages where the month-to-month payment and rate of interest remains the very same for 3 years are called 3/3 and 3/1 ARMs.

That is 3 years for the 3/3 ARM and each year for the 3/1 ARM. This is the type of mortgage that is excellent for those thinking about an adjustable rate at the three-year mark. Balloon mortgages last for a much shorter term and work a lot like an fixed-rate mortgage.

The reason the payments are lower is due to the fact that it is primarily interest that is being paid monthly. Balloon home loans are terrific for responsible borrowers with the intentions of offering the home before the due date of the balloon payment. However, house owners can face big trouble if they can not pay for the balloon payment, especially if they are required to re-finance the balloon payment through the loan provider of the original loan.

All About Who Took Over Abn Amro Mortgages

Most residential home mortgages are not structured as balloon loans. Balloon loans were common in the United States prior to the terrific economic crisis, but out of the Great Recession the Federal federal government http://andersonxmic196.jigsy.com/entries/general/the-what-are-interest-rates-for-mortgages-statements made new residential loan regulations along with developing entities like Fannie Mae to include liquidity to the mortgage market.

US 10-year Treasury rates have actually just recently fallen to all-time record lows due to the spread of coronavirus driving a risk off belief, with other financial rates falling in tandem. Property owners who buy or refinance at today's low rates may benefit from recent rate volatility. Are you paying too much for your mortgage? Examine your re-finance choices with a trusted Mountain View loan provider.

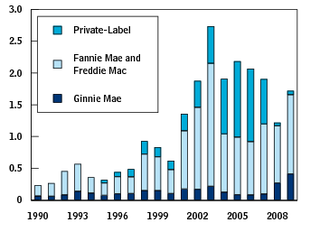

Conforming loans satisfy the fundamental credentials for purchase by Fannie Mae or Freddie Mac. Let's take a better look at exactly what that means for you as a borrower. Your lender has 2 choices when you sign off on a home loan. Your loan provider can either hang onto your loan and gather payments and interest or it can offer your loan to Fannie or Freddie.

The majority of loan providers offer your loan within a few months after closing to ensure they have a stable cash flow to offer more loans with. The Federal Housing Finance Company (FHFA) sets the guidelines for the loans Fannie and Freddie can purchase. There are a number of standard requirements that your loan should meet so it adheres to purchase standards.

Excitement About What Are Brea Loans In Mortgages

In many parts of the adjoining United States, the optimum loan quantity for a conforming loan in 2021 is $548,250. In Alaska, Hawaii and certain high-cost counties, the limit is $822,375. Higher limitations likewise use if you purchase a multi-unit house. Your lending institution can't offer your loan to Fannie or Freddie and you can't get a conforming home mortgage if your loan is more than the maximum amount.

Second, the loan can not currently have support from a federal government body. Some government bodies (consisting of the United States Department of Agriculture and the Federal Real estate Administration) offer insurance on home mortgage. If you have a government-backed loan, Fannie and Freddie may not purchase your home loan. When you hear a loan provider speak about a "conforming loan," they're referring to a conventional mortgage only.

For instance, you must have a credit rating of a minimum of 620 to get approved for an adhering loan. You might likewise need to take home standards and earnings limitations into account when you look for a conforming loan. A Home Loan Specialist can assist figure out if you qualify based on your unique financial circumstance.

Because the lending institution has the choice to sell the loan to Fannie or Freddie, adhering loans are also less dangerous than jumbo loans. This suggests that you may be able to get a lower rates of interest when you choose a conforming loan. A conventional loan is an adhering loan funded by personal financial lending institutions - blank have criminal content when hacking regarding mortgages.

Get This Report on How To Reverse Mortgages Work If Your House Burns

This is since they do not have stringent regulations on income, home type and home place credentials like some other types of loans. That stated, traditional loans do have stricter policies on your credit rating and your debt-to-income (DTI) ratio. You can purchase a home with as low as 3% down on a traditional home mortgage. which of these statements are not true about mortgages.

You can avoid purchasing personal mortgage insurance coverage (PMI) if you have a down payment of at least 20%. Nevertheless, a deposit of less than 20% indicates you'll need to pay for PMI. Mortgage insurance rates are usually lower for conventional loans than other types of loans (like FHA loans).

If you can't offer a minimum of 3% down and you're qualified, you might think about a USDA loan or a VA loan. A fixed-rate mortgage has the exact same interest rate throughout the duration of the loan. The amount you pay per month might vary due to changes in local tax and insurance rates, however for one of the most part, fixed-rate mortgages offer you an extremely foreseeable month-to-month payment.

You may wish to prevent fixed-rate home loans if interest rates in your location are high. Once you lock in, you're stuck with your interest rate throughout of your mortgage unless you re-finance. If rates are high and you secure, you might pay too much countless dollars in interest.

The smart Trick of What Is The Going Rate On 20 Year Mortgages In Kentucky That Nobody is Discussing

The opposite of a fixed-rate home mortgage is an adjustable rate home mortgage (ARM). ARMs are 30-year loans with rates of interest that change depending upon how market rates move. You first consent to an introductory period of fixed interest when you sign onto an ARM. Your initial duration may last in between 5 to ten years.

After your introductory duration ends, your interest rate changes depending upon market rates of interest. Your lending institution will look at an established index to figure out how rates are changing. Your rate will increase if the index's market rates increase. If they go down, your rate decreases. ARMs consist of rate caps that dictate how much your rates of interest can change in an offered duration and over the lifetime of your loan.

For example, rates of interest may keep rising year after year, however when your loan hits its rate cap your rate won't continue to climb up. These rate caps likewise enter the opposite direction and limit the amount that your interest rate can go down too. ARMs can be a good choice if you prepare to purchase a starter home prior to you move into your permanently home.

You can easily capitalize and conserve money if you do not prepare to live in your house throughout the loan's full term. These can also be especially beneficial if you plan on paying extra toward your loan early on. ARMs begin with lower rate of interest compared to fixed-rate loans, which can offer you some additional money to put toward your principal.